Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Luxury Living with Sweeping Southwest Views

Welcome to a truly exceptional retreat where luxury, privacy, and breathtaking natural beauty come together. Overlooking the sparkling waters of Clear Lake and Beaver Lake, this upscale home offers panoramic southwest-facing lake, territorial, and mountain views. It is here that you will experience the kind of views that turn everyday moments into something extraordinary. Set on 5 private acres in Skagit County just 10 minutes away from Big Lake. This property delivers the rare balance of peaceful seclusion with the convenience of being just minutes from nearby cities. This is more than a home. It’s a lifestyle designed for comfort, entertaining, and year-round enjoyment. If this sounds like everything you have been looking for, keep reading to discover luxury living with sweeping Southwest views over clear lake and Beaver Lake.

A Refined Main Level Designed for Everyday Living

The main level welcomes you with elegant yet functional spaces that flow seamlessly together. At the heart of the home is the gourmet kitchen, thoughtfully designed for both serious cooking and casual gatherings. Set the stage for effortless entertaining with marble countertops, a custom-built walk-in pantry with extra lighting and a glass door, and premium appliances. Appliances like a Sub-Zero refrigerator and Wolf range and dishwasher.

The kitchen connects naturally to a warm living space anchored by a gas fireplace and HD TV, creating a perfect spot to relax or host friends. The formal great room adds flexibility for larger gatherings. A dedicated office provides a quiet space to work from home. Just off the garage is a laundry room, complete with a sink and additional pantry storage that adds everyday convenience without sacrificing style.

Lower-Level Entertainment at Its Finest

Downstairs, the home transforms into an entertainer’s dream. Movie nights become unforgettable in the private home theater. The theater features an upgraded projector, 10 plush leather seats, and a 100-inch screen. Adjacent is a spacious game and entertainment room that includes an electronic foosball table, full size shuffleboard table, and two mounted LED TV’s for game days with a fully equipped wet bar, including an ice maker, refrigerator, and dishwasher. Can you imagine yourself hosting everything from game days to intimate gatherings yet?

Ever describe yourself as a wine enthusiasts? If so, you will appreciate the wine cellar and tasting room. These rooms showcase rich wood wine racks and a stunning marble tasting table with a copper lined waterfall sink in the center. A private sauna adds a spa-like touch, while the independent built-in sound system throughout the lower level of the home and expands out across the deck to ensure the perfect ambiance in every space.

Upper-Level Comfort and Flexibility

The upper level offers a peaceful retreat at the end of the day. The primary suite is spa-inspired, featuring a jetted soaking tub, separate shower, double sinks, and generous his-and-hers closets. Two additional large bedrooms with spacious closets provide comfort for family or guests. Additionally, a versatile rec room can easily serve as an overnight guest space, game room, or creative studio. Bathrooms feature elegant travertine tile flooring, adding timeless appeal. Contributing to the luxurious experience is an intercom system that allows for easy communication between the upper and main levels.

Outdoor Living with Unmatched Views

Step outside and take in the views from over 1,500 square feet of multi-level decking, perfectly positioned to capture stunning sunsets and sweeping lake vistas. Relax in the hot tub, recently upgraded with a new motor and treated with salt enzymes, or enjoy summer evenings with friends thanks to the plumbed gas line for your BBQ.

A fenced dog run and fully fenced backyard provide peace of mind for pet owners, while the surrounding natural setting offers frequent sightings of local wildlife—adding to the sense of escape and tranquility.

Thoughtful Upgrades & Peace of Mind

This home is equipped with features that enhance comfort and reliability year-round, including:

- Generac whole-home generator for uninterrupted power during inclement weather

- New furnace (2022)

- New on-demand hot water heater (2022)

- Propane-fueled systems that ensure heat and fireplace use even during outages

According to the current owners, the privacy, wildlife, and ability to enjoy world-class amenities without being in the heart of a major city are what truly make this home special.

A Rare Clear Lake Opportunity

Built in 1990, this two-story home with a basement offers timeless craftsmanship paired with modern luxury. Located in the Sedro-Woolley School District, it’s a rare opportunity to own a private retreat that feels worlds away—yet remains conveniently close to everything Skagit County has to offer.

Get the rest of the details here.

If you’re searching for luxury living with sweeping Southwest views, let’s connect! This Clear Lake retreat is ready to welcome you.

This home is listed by: Becky Elde

The North Cascades

Wild Beauty Meets Endless Wonder in the North Cascades. If you have ever taken Highway 20 or stood at a lookout along the North Cascades Scenic Byway, you have experienced the difference. It is more dramatic, raw, and rugged than just about anywhere else in Washington. What makes The North Cascades so different? They aren’t just mountains! They are one of the most spectacular landscapes in North America. The product of being carved by ice, shaped by time, and wrapped in a sense of wildness that is difficult to describe but impossible to forget once experienced.

Welcome to the North Cascades: the “American Alps” that live up to their name in every way.

A Landscape Carved by Time and Ice

The North Cascades are some of the most rugged mountains in the continental United States. There’s a reason for that! For millions of years, glaciers have scraped, sculpted, and carved this region into sharp ridgelines, jagged peaks, plunging valleys, and steep-walled canyons.

It’s this geologic history that gives the range its dramatic appearance:

- Craggy peaks that cut into the sky

- Deep turquoise lakes fed by glacial runoff, like Diablo Lake

- U-shaped valleys formed by massive sheets of ice

- Waterfalls that appear to tumble from nowhere

Counts cite over 300 glaciers! For reference, North Cascade glaciers make up nearly a third of all glaciers found in the lower 48 states. By far, the largest collection in the Lower 48. These glaciers continue shaping the landscape today, leaving behind the striking blues and rocky textures the North Cascades are known for.

A Wilderness of Pines, Snow, and Untamed Beauty

The North Cascades are home to dense forests of cedar, fir, and pine that cling to the slopes and fill the valleys below. As you approach the higher elevations, the trees give way to wildflower meadows, windswept ridges, and snowy peaks that remain frosted long into summer.

It is here; you find:

- Towering evergreens that fill the air with the scent of resin and rain

- Snowfields and glaciers that glow blue in the afternoon light

- Wildlife like black bears, marmots, mountain goats, and soaring eagles

- Alpine lakes so clear that they reflect the peaks like glass

The North Cascades are remote enough to feel untouched, yet accessible enough that anyone can experience moments that feel like pure wilderness escape.

The North Cascades Highway: A Drive Like No Other

If there is one thing that elevates this mountain range even further, it’s the drive.

Highway 20 (the North Cascades Scenic Byway) is often called one of the most beautiful drives in the country. For good reason, every switchback and overlook reveals something new:

- The emerald waters of Diablo Lake

- The towering spires of Liberty Bell Mountain

- The vast, layered ridgelines stretching endlessly into the horizon

- Rivers, forests, and valleys that change color with every season

Whether you are stopping at lookouts, hiking a trail, or simply soaking in the view from your car window, the drive offers a sense of awe that builds mile after mile.

Fall lights up in fiery colors of oranges and golds. Winter wraps the peaks in white. Spring returns with roaring waterfalls, and summer unveils the full glory of alpine blue skies. No matter when you visit, the North Cascades feel like a new place every time.

What Makes the North Cascades So Special?

It’s a combination of drama, solitude, and sheer natural beauty. It is the feeling of seeing mountain after mountain fade into the distance, knowing most of them are untouched wilderness. It’s the sense that the land is old, powerful, and yet still shaping itself.

The North Cascades are special because they remind us of something rare:

There are still places where nature feels truly wild.

Thinking about calling the PNW home? Let’s Connect!

Winter’s Most Magical Visitors

Every fall, as the air cools and the fields between Mount Vernon and Anacortes turn golden and quiet, something extraordinary happens. The snow geese return gracing our skies and our fields. For months, drivers along Fir Island Road, Highway 20, and the backroads between Conway and La Conner are treated to one of the Pacific Northwest’s most spectacular natural events. Thousands upon thousands of brilliant white birds gather across the farmland. To experience it is like a living snowstorm settling on the fields.

They’re impossible to miss, and even harder to forget.

Who Are These Majestic White Birds?

These annual visitors Snow Geese. These birds are famous for their striking white bodies, jet-black wingtips, and soft pink bills. They are part of one of the largest migratory waterfowl populations in the world.

Snow geese spend their summers nesting in the Arctic tundra, from Alaska to Siberia. As winter approaches food begins to grows scarce. In response, they travel thousands of miles south in enormous flocks. Sometimes you will see them flying in the classic V-shape and other times traveling in swirling clouds of white until they reach the mild, food-rich lowlands of Washington.

Year after year, they have choose Skagit Valley as one of their favorite places to rest and feed.

Why Do Snow Geese Come to Skagit Valley?

Skagit Valley is a paradise for wintering geese. The landscape between Mount Vernon and Anacortes provides exactly what they need:

🌾 Open Farmland

Harvested agricultural fields leave behind residual grain, roots, and plant material making for an ideal buffet for hungry geese after their marathon migration.

🕊 Safe Gathering Space

Vast open spaces give flocks room to land, rest, and take off again with ease. The ability to see predators coming from all directions makes the valley especially attractive.

💧 Wetlands & Marshes

Nearby areas like the Skagit Flats, Padilla Bay, and the restored wetlands on Fir Island create the perfect environment for feeding, roosting, and preening.

🌤 Mild Winter Climate

Compared to the frozen Arctic, Skagit’s cool but temperate winter provides a comfortable refuge.

All of these combined creates the perfect seasonal home for snow geese. That’s why thousands upon thousands of snow geese return here every year, usually from October through March. To learn more about these magical visitors read this article: Snow Geese of the Pacific Flyway.

A Natural Spectacle You Don’t Want to Miss

Whether you are commuting between cities or intentionally going “geese chasing,” the experience is unforgettable.

Often you will see:

-

Giant flocks blanketing entire fields like a fresh layer of snow

-

Sudden eruptions of wings and sound making a thunderous “whooosh” as thousands lift off at once

-

Spiraling clouds of white birds sweeping across the sky

-

Black-tipped wings flashing as they move in synchronized waves

And sometimes, right before they land, they hover, feet dangling, wings fanned wide. In this moment they almost look as if they are moving in slow motion. It is like nothing else you’ve ever experienced before.

Photographers, birdwatchers, and families come from all over the region for the chance to witness scenes like these. For locals, it’s one of the many things that makes living in Skagit Valley so special.

How to See Them Up Close

You can spot snow geese reliably in these areas:

-

Fir Island (the most famous viewing location)

-

Between Conway and La Conner

-

Fields along Highway 20

-

Skagit Flats near Bay View and Edison

Just be sure to pull fully off the road, stay respectful of private property, and give the birds plenty of space to feed and rest.

A Seasonal Reminder of Why We Love Where We Live

For several months each year, snow geese turn our everyday drives into something magical. Their presence transforms simple farm fields into scenes worthy of a wildlife documentary. Winter’s most magical visitors remind us that Skagit Valley is full of wonder, even in the quietest seasons.

It’s one more reason to take the scenic route. One more reason to slow down. One more reason to appreciate the place we’re lucky enough to call home.

If you have come to witness this magic and have determined you want to call it home, connect with us we are happy to help you make your PNW living dreams come true.

Coastal Beauty Meets Everyday Adventure

Anacortes is one of those rare places where the line between everyday life and vacation living feels beautifully blurred. It is a place where coastal beauty meets everyday adventure. The mornings begin with golden light stretching over the water. The afternoons welcome long walks on forested trails. Last but not least, the evenings often end with sunsets that paint Burrows Bay in shades of rose and gold.

From the salty breeze off the marina to the vibrant local arts scene, there’s a rhythm to life in Anacortes that feels both invigorating and deeply grounding. Spend a Saturday discovering shops and cafés downtown, hop aboard a whale-watching tour, explore miles of scenic hiking in the nearby Anacortes Community Forest Lands, or launch your kayak into the glassy waters of the bay. When your heart desires to explore a little further, you are just a ferry ride away.

What truly makes Anacortes special is the lifestyle it has to offer. A lifestyle that blends natural beauty with a strong sense of community. Neighborhoods like Skyline that bring people together around beaches, sports courts, parks, clubhouses, and cabana with a shared love of the water. It’s an area designed for those who want to live close to the shoreline and even closer to adventure.

A Home That Amplifies the Anacortes Lifestyle

If you are thinking about making Anacortes your home and have ever dreamt of living where your home is as adventure-ready as you are, perhaps this updated Skyline property would do just that for you. 2016 Piper Circle Anacortes Listed by: Julie Birkle.

Boasting breathtaking views of Burrows Bay, the Olympic Mountains, and unforgettable sunsets, this 3,500+ SF home captures the essence of coastal living. Inside, you will find thoughtful upgrades throughout. Upgrades like granite kitchen counters, new appliances, refreshed bathrooms, a cozy gas fireplace, new windows, siding, decks, and fresh exterior paint. Modern comforts include a whole-house generator, tankless water heater, and a security system for peace of mind.

But one of the standout features is the incredible amount of parking and storage. This is a true rarity in the Pacific Northwest coastal market.

Space for Everything: RVs, Boats, Cars, and All Your Toys

Whether you are an RVer, a boater, an explorer, or all three, this home is built for the lifestyle.

-

Generous RV parking with dedicated sewer and power hookups

-

Room for a large RV, boat, toy hauler, or trailer

-

Additional off-street parking for multiple vehicles

-

Minutes from the Skyline Marina and boat launch

Imagine the ease of stepping out your door, loading up your gear, and heading straight to the mountains or the water with no hassle. This home offers no storage hassles, no off-site parking fees, no extra stops. This home quite literally puts adventure at your doorstep.

When you find yourself ready to stay close to home, enjoy Skyline’s exclusive amenities: a private beach, sports courts, parks, clubhouse, cabana, and the waterfront just a short stroll away.

Ready to Live the Anacortes Lifestyle?

If your heart belongs to the Pacific Northwest for its water, its wilderness, its slow coastal days paired with spontaneous adventure, this home offers the perfect place to plant roots.

With room for every vehicle, every toy, and every future plan, it’s more than a home.

It’s your launch point for life in Anacortes. Let’s Connect.

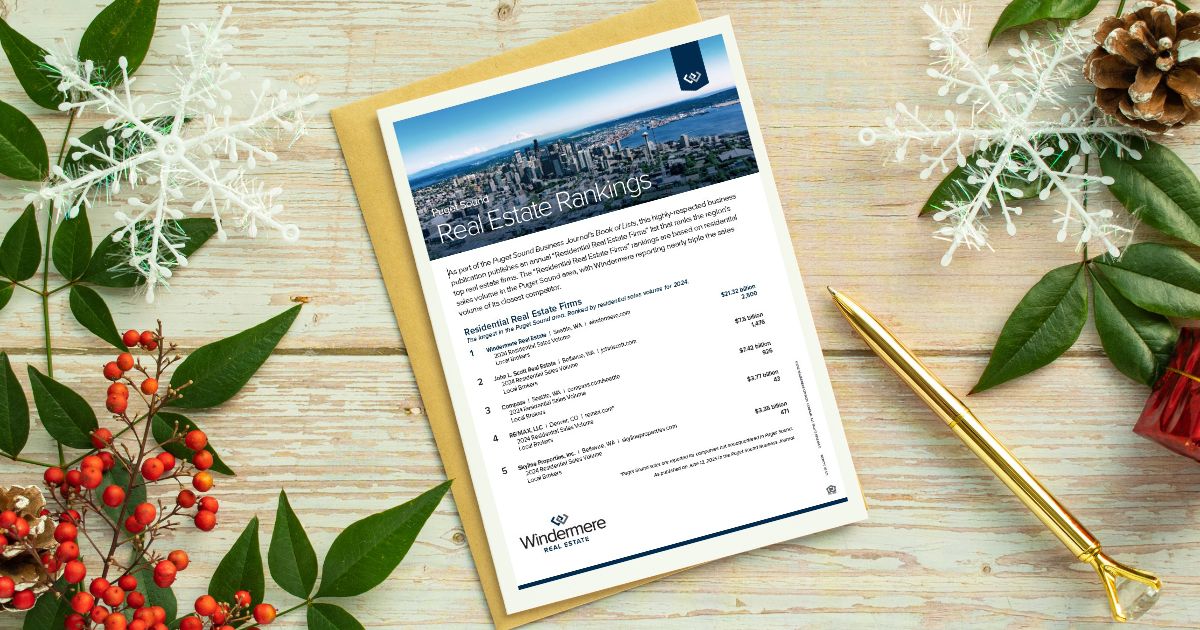

A Legacy of Market Leadership

We were thrilled to see the Puget Sound Business Journal’s most recent real estate rankings (check them out here). Windermere has been a legacy of market leadership in the Puget Sound. The report supports this by demonstrating how Windermere Real Estate continues to assert its position as the foremost residential real estate firm in the Puget Sound region. Reporting $21.32 billion in residential sales volume. Windermere’s performance outpaces its nearest competitor by nearly a threefold margin. This information reinforces Windermere’s longstanding dominance in the regional housing market.

The history:

The Puget Sound Business Journal inaugurated its list of top residential real estate companies in 1986. Windermere has maintained the No. 1 ranking every single year. This nearly four-decade tenure highlights not only Windermere’s market share but its sustained organizational resilience, strategic adaptability, and strong community presence. We are extremely proud to be a part of it.

Factor of Success:

Several factors contribute to Windermere’s enduring success. First, its expansive network across the Pacific Northwest supports unparalleled market coverage and client reach. Second, the emphasis on agent education, technological integration, and customer-centered service has strengthened its professional reputation and operational efficiency. Finally, Windermere’s deep-rooted commitment to community engagement. The Windermere Foundation, funded in part by a portion of every home sold distinguishes Windermere as both a market leader and a socially responsible organization. As Windermere offices and agents in the Puget Sound, we couldn’t be more proud.

Here is a snip-it into what our Anacortes, Sedro-Woolley, Skagit Valley, and Arlington offices have been doing in our communities recently:

What it all means:

Windermere’s continued ability to outperform their competitors at such scale suggests a robust alignment between regional market demands and Windermere’s business model. Housing markets across the Puget Sound area evolve in response to demographic shifts, economic pressures, and ongoing development patterns. Windermere’s legacy of leadership positions it uniquely to shape the future trajectory of real estate services in the region.

In sum, Windermere’s top ranking is not merely a reflection of annual sales. Windermere’s top ranking is a testament to nearly forty years of consistent excellence, strategic foresight, and unwavering commitment to all of the communities served. We are grateful for your continued trust in our services and look forward to continuing to serve you for years to come.

If you are looking to making a move in your future please reach out. We would love to help you. If you wish to have a copy of this document mailed or emailed to you please email us at northsound@windermere.com.

Discover the Magic of Diablo Lake

Nestled in the rugged wilderness of the North Cascades, discover the magic of Diablo Lake. Diablo Lake is one of Washington’s most breathtaking destinations. It is a special place where turquoise waters meet dramatic mountain peaks, and every turn along the highway feels like you are stepping into a postcard. You will find Diablo Lake just east of the charming Skagit Valley communities. This natural wonder makes for the perfect day trip or weekend adventure for locals and visitors alike.

The Magic Behind the Color

One of the most captivating things about Diablo Lake is its brilliant blue-green color. The vibrant hue comes from “glacial flour”. A phenomenon where fine rock particles created by glaciers grinding against stone stay suspended in the water. When the sunlight reflects off the particles it creates the surreal blue-green tone of lake with an almost otherworldly glow. You must see it to believe it.

Things to Do Around Diablo Lake

Whether you are an adventurer, photographer, or someone looking for a peaceful escape, there is something for everyone.

Hiking:

Explore the popular Diablo Lake Trail, a 7.2-mile trail with stunning viewpoints of the lake and surrounding peaks. The complete trail includes an elevation gain of 1,509 feet and generally takes about 3.5 to 4 hours to complete.

Boating & Kayaking:

During peak seasons you can rent a kayak or join a guided boat tour to experience the lake from the water and learn about the area’s fascinating history.

Picnicking:

The Diablo Lake Overlook offers one of the most scenic picnic spots in the state. Don’t just drive by, this is a must-see for anyone driving along Highway 20. Pack a lunch and stop to enjoy the view.

Camping:

If you plan for an extended stay, there are nearby campgrounds like Colonial Creek that offer the chance to fall asleep under a blanket of stars, surrounded by the sounds of nature.

A Connection to Home

For those who call the Skagit Valley, or the surrounding areas home, Diablo Lake is more than just a destination, it is a reminder of why we live here. The North Cascades showcase the incredible balance between wild beauty and accessible adventure that makes the Pacific Northwest lifestyle so special.

Diablo is a place that inspires gratitude for the land we live on and the communities that protect it. Whether you are new to the area or a lifelong resident, taking the time to explore places like Diablo Lake deepens your connection to this incredible corner of the world.

Real Estate and the PNW Lifestyle

Living near places like Diablo Lake means having nature’s playground right in your backyard. For homebuyers seeking both tranquility and adventure, properties in Skagit and Snohomish Counties offer a gateway to this lifestyle. Those lucky enough to live here can enjoy weekends spent hiking mountain trails or relaxing by the water. Every season brings new reasons to fall in love with the Pacific Northwest.

Ready to Find Your PNW Home?

If the idea of living close to scenic trails, alpine lakes, and charming small towns sounds like your dream, let’s connect. We would love to help you discover a home that fits your lifestyle, whether that is a cozy cabin tucked among the trees or a home with a view of the mountains that make this region so magical.

📞 Reach out today to learn more about homes near the North Cascades, or explore listings across Skagit and Snohomish communities.

Celebrating Día de los Muertos

Honoring Life and Tradition

Día de los Muertos, or Day of the Dead, is a vibrant tradition celebrated primarily on November 1st and 2nd across Mexico and by communities around the world. This celebration is far from a somber occasion. Instead it is a joyful celebration of life, memory, and family. It is a dedicated time to honor and remember loved ones who have passed. Join us in celebrating Día de los Muertos through understanding its roots, sharing the traditions, and celebrating with local events.

The History and Meaning

The roots of Día de los Muertos stretch back thousands of years to Indigenous cultures of Mesoamerica, including the Aztec, Maya, and other pre-Columbian civilizations. These early communities believed in the cyclical nature of life and death, honoring ancestors through rituals and offerings. When Catholicism arrived with Spanish colonization, the holiday merged with All Saints’ Day and All Souls’ Day, creating the unique tradition we see today.

At its heart, Día de los Muertos is about connection. Many families build altars (ofrendas) that are decorated with photos, candles, marigolds, and favorite foods of the departed. Sugar skulls, papel picado, and other colorful decorations help create a festive, celebratory atmosphere.

Traditions and Celebrations

Across communities, celebrations include:

-

Ofrendas: Altars that honor loved ones, often with personal items, photos, flowers, and food.

-

Marigolds (Cempasúchil): Known as the flower of the dead, their bright color and scent are believed to guide spirits back to the living.

-

Sugar Skulls (Calaveras): Sweet, decorative treats that celebrate the uniqueness of each life.

-

Food & Gatherings: Families prepare favorite dishes of those who have passed and share them in remembrance.

-

Parades & Festivals: Music, dance, and colorful processions often mark the public celebration of the holiday.

A Celebration of Community

Día de los Muertos is more than a personal remembrance, it’s a cultural celebration that strengthens community bonds. Many cities across the U.S., including in the Pacific Northwest, host public festivals and events to honor these traditions. It’s an opportunity to learn, share stories, and participate in a rich cultural heritage.

Here are a few happening right here in Skagit, Snohomish, and Island County:

-

Day of the Dead at Lynnwood Library (Snohomish)

- Dia de Los Muertos – Wallin-Stucky Funeral Home (Island)

-

Dia De Los Muertos Sound Bath (Island)

Reflection and Appreciation

Participating respectfully in Día de los Muertos encourages us to reflect on life, legacy, and memory. Whether you are visiting a local celebration, creating a small altar at home, or learning the history of the holiday, this season reminds us of the importance of honoring those who came before us while celebrating the present.

If you have enjoyed reading this article and wish to connect with us, please connect with us here.

Make Shorter Days Work For You and Your Home

When the clocks turn back and daylight fades a little earlier, life in Skagit and Snohomish takes on a cozier rhythm. The fields, forests, and towns glow in fall colors. The evenings become an invitation to slow down and enjoy the comforts of home. This article will help you embrace the season and learn how to make shorter days work for you and your home.

A Seasonal Shift with a Purpose

Originally, Day Light Savings was created to maximize daylight hours. While “Falling back” is not always welcomed with an abundance of joy, it does offer a reminder that every season brings its own kind of productivity. “Falling back” gives us a bit more morning light. This early light offers us a great excuse to refocus on the spaces we spend the most time in.

Indoor Inspiration

As evenings begin to grow darker, we are provided the perfect opportunity to make our homes feel brighter and more functional. Here are a few ideas to help.

Refresh Your Entryway:

Try adding hooks for coats, a doormat for rainy-day shoes, and soft lighting to create a welcoming first impression.

Cozy Corners:

Layer textures with throw blankets, pillows, and rugs to make living spaces warm and inviting.

Brighten with Color:

Incorporate autumn tones like amber, rust, or olive in decor. These small changes add warmth to shorter days.

Clean & Prep:

Use that “extra hour” to tackle small projects before the holidays — clean windows, deep-clean the kitchen, or declutter high-traffic areas. *Pro tip: Winter is coming start planning for winterizing your home now.

Real Estate Reflections

Even as daylight fades, the housing market keeps moving. Buyers touring in the evening will notice how well a home feels at dusk. The soft lighting, a pleasant scent, and tidy organization all make a difference for how the home feels. Sellers can use this season to stage their homes for warmth and comfort, appealing to the desire for a welcoming space as winter approaches.

As we “fall back,” remember that shorter days don’t have to mean less light. It just means we shift where we find it. Whether it’s in your home, your community, or a new chapter ahead, there’s always something to brighten the season. If you are thinking about buying or selling, let’s connect!

Discover the Anacortes Beached Boat

A Day-Trip Treasure

When you’re exploring Anacortes, it’s easy to get swept away by the sparkling waters, island views, and charming downtown. However, tucked along the Guemes Channel Trail, discover the “Anacortes Beached Boat”. A hidden gem that’s equal parts history, nature, and Pacific Northwest quirk: the famous beached boat—officially known as the La Merced.

A Ship With Stories to Tell

The La Merced isn’t just any old vessel. Built in 1917 as a four-masted schooner for Standard Oil, she once carried petroleum products across the seas during the World War I era. Later, she was transformed into a floating cannery, working the Alaskan waters before finding her final resting place in 1966 at Lovric’s Boatyard on Fidalgo Island.

Rather than sail off into obscurity, the La Merced was scuttled and repurposed as a breakwater, protecting the boats in the marina from rough waters. And while her sailing days are long gone, she’s taken on a new kind of life.

Where History Meets Nature

Today, the La Merced is more than a shipwreck—it’s a forest on the water. Over the decades, trees and wildlife have taken root within her hull, turning this maritime relic into a floating ecosystem. It’s a rare sight: a schooner-turned-sanctuary where history and nature intertwine.

Because of her unique past and enduring presence, the La Merced was officially added to the National Register of Historic Places in 1990.

How to See It

If you’d like to experience this Anacortes landmark for yourself, the best view is from the Guemes Channel Trail, not far from the San Juan Islands ferry terminal. You can also catch a closer look from the adjacent marina parking lot, though remember—it’s an active boatyard, so be respectful of the space.

Why It’s Worth the Stop

The Anacortes Beached Boat isn’t just a landmark; it’s a reminder of how places—and vessels—can evolve over time. What once carried petroleum and canned salmon now holds trees, birds, and stories. It’s the kind of stop that adds a little wonder to your day trip, and one more reason to fall in love with the charm of Anacortes.

Whether you’re walking the trail, waiting for the ferry, or simply searching for something memorable to do in town, the La Merced is a must-see slice of PNW history.

If you loved this and are dying to learn more about our beautiful PNW area connect with us.

If you discover the Anacortes Beached Boat and wish to share your adventure tag us at @Windermere_Anacortes

Windermere E3

A reflection of our 2025 Windermere E3: Engage, Energize, Elevate event.

At Windermere, growth isn’t just about closing transactions. It is about elevating the experience for everyone involved, from our agents to our clients and communities. We grow together to better serve you. That spirit of growth and connection was at the heart of our recent Windermere E3 event held at the beautiful Suncadia in Cle Elum. Agents from across the region came together for a few unforgettable days of education, collaboration, and celebration.

Why being part of Windermere is so special

From networking to dancing the night away, the event was a vibrant reminder of what makes being a part of Windermere so special. Together we share a commitment to learning, supporting one another, and serving our clients with excellence.

Lead by the best in the industry to better serve you

Throughout the event, agents engaged in insightful sessions led by some of the best in the industry. Sharing strategies to enhance communication, improve client care, and stay ahead in a constantly evolving market. Every conversation, breakout session, and connection was focused on one goal: how to provide a better experience for the buyers and sellers we serve.

Supporting community needs

Beyond education, we also came together to give back. Together we raised $22,000 through live and silent auctions to support homeless families in need. It was a powerful example of how collaboration and compassion go hand in hand at Windermere.

When you work with a Windermere agent, you are not just working with a real estate professional. You are partnering with someone who is continually learning, evolving, and striving to deliver the highest level of service. Because when we engage, energize, and elevate each other, we elevate the entire experience of buying or selling a home.

A heartfelt thank you to everyone who made Windermere E3 possible. A special thank you to Shawna Ader for creating such an inspiring and impactful event.

At Windermere, we don’t just sell homes. We build relationships, strengthen communities, and continually push ourselves to be better for you.

If you are considering buying or selling and are in need of a real estate professional by your side, connect with us.